USAA Auto Insurance Guide [Everything You Need]

Free Car Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Jeffrey Johnson

Insurance Lawyer

Jeffrey Johnson is a legal writer with a focus on personal injury. He has worked on personal injury and sovereign immunity litigation in addition to experience in family, estate, and criminal law. He earned a J.D. from the University of Baltimore and has worked in legal offices and non-profits in Maryland, Texas, and North Carolina. He has also earned an MFA in screenwriting from Chapman Univer...

Insurance Lawyer

UPDATED: Sep 12, 2019

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident auto insurance decisions. Comparison shopping should be easy. We are not affiliated with any one auto insurance provider and cannot guarantee quotes from any single provider. Our partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance-related. We update our site regularly, and all content is reviewed by auto insurance experts.

UPDATED: Sep 12, 2019

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident auto insurance decisions. Comparison shopping should be easy. We are not affiliated with any one auto insurance provider and cannot guarantee quotes from any single provider. Our partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

On This Page

| USAA Company Overview | Info |

|---|---|

| Year Founded | 1922 |

| Current Executives | Stuart Parker, Chief Executive Officer Laura Bishop, Executive Vice President and Chief Financial Officer |

| Number of Employees | 33,786 |

| Total Sales/Assets | 155.4 billion |

| HQ Address | 9800 Fredericksburg Rd. San Antonio, TX 78288 |

| Phone Number | 800-531-8722 |

| Company Website | https://www.usaa.com |

| Premiums Written (Total Private Passenger Auto) | 14,467,936 |

| Loss Ratio | 0.77% |

| Best For | Auto Insurance Homeowners Insurance Renters Insurance Life Insurance Umbrella Insurance Medicare Health, Dental, and Vision Insurance |

It all began in 1922.

A group of 25 military officers combined their business acumen and innovation to found the United Services Automobile Association or USAA. The company was started in San Antonio as a way for these 25 Army officers to insure each other’s cars, and they had no idea that the entity would skyrocket into the thriving insurance giant it is today.

Fast forward to today, with assets totaling in the billions and tens of thousands of employees spread across the nation, USAA provides a wide range of financial services to current and former military members and their families, from auto and home insurance to banking and retirement products.

Whether you’re a longtime customer of USAA or are considering purchasing coverage through this insurer for the very first time, this one-stop-shop USAA auto insurance review is most certainly for you.

Our team understands how time-consuming (and frankly, stressful) searching for auto insurance can be.

But, it doesn’t have to be.

From the ratings that top agencies like AM Best and Moody’s have awarded USAA to the carrier’s future outlook to its average annual rates by factors such as your commute and driving record — we’ve got it all here for you.

Simplify your search for coverage today when you use our FREE online quote tool. Enter your zip code in the box above to get started.

Are you ready? Let’s jump right into our USAA auto insurance review.

Rating Agencies

One of the very first components you should assess when determining whether or not a carrier is the best fit for your insurance needs is their ratings. If you’re not sure where to find these types of ratings — no need to worry, we’ve got you covered.

Renowned independent agencies such as J.D. Power and S&P regularly publish ratings for various insurance companies throughout the country. The reason a carrier’s ratings matter so much is that they reveal two primary things.

First, ratings indicate the financial state and creditworthiness of a carrier, which is a measuring stick for how likely the company is to continue fulfilling its financial obligations to consumers. Second, ratings reveal whether or not consumers are satisifed overall with the company’s services.

Sounds like something you need to know, right? Let’s get down to business.

– AM Best

AM Best’s system of rating insurance companies is highly looked up to by both carriers and consumers everywhere — and with good reason. A positive or negative rating from AM Best could be the deciding factor as to whether or not a potential insured decides to purchase coverage or go with a competitor.

AM Best has awarded USAA a financial strength rating of A++, which is the highest rating they award to any insurer. A rating of A++ indicates that the company has a superior ability to continue to meet their obligations to insureds.

Furthermore, AM Best assigned USAA a Long-Term Issuer Credit Rating of aaa, which is also the top rating they designate to any carrier. An aaa rating symbol indicates that the entity has an exceptional ability to meet their consumer obligations.

Long story short, this is good news for both USAA and anyone considering taking out a policy with this insurer.

Now, let’s take a look at what the Better Business Bureau has to say about USAA.

Better Business Bureau

The Better Business Bureau or BBB is a non-profit organization that issues rankings for companies based on their unique Accredited Business System. To be clear, the BBB is not affiliated with any government entities, but they are a dependable and premier source that customers can look to identify a company’s ratings.

We would like to note, that the BBB assigns ratings to companies based on the state they are located in, with ratings assigned to individual offices in various cities. For instance, in San Antonio, Texas where the company is headquartered, USAA has a rating of B-.

The BBB uses a 100 point scoring scale when designated letter grade ratings to a particular company. A rating of B- would indicate an overall score of 80. It is also important to note, that you should never use any single agency’s ratings to determine your choice of an insurer.

Only by reviewing multiple ratings from different agencies can you draw an informed conclusion regarding whether the company is best suited to your specific insurance needs.

The BBB’s ratings take a number of elements into account, including the following:

- The company’s complaint history with the BBB

- The type of company

- The length of time the company is been in business

- The transparency of the company’s business practices

- If the company has failed to honor any commitments to the BBB

- Any advertising issues the company has that are known to the BBB

Moody’s Rating

Moody’s rating scale diverges somewhat from AM Best’s and the BBB’s in the sense that they use a letter grade scale ranging from Aaa to C. The highest rating Moody’s awards is Aaa, with the C being the lowest indicator assigned.

Interestingly enough, in March 2019, while Moody’s assigned USAA an Aaa rating, they also projected a negative outlook for the company. This was a change from the stable outlook Moody’s reported for USAA as recently as December of 2018.

The Aaa rating is a long-term rating, indicating that USAA’s obligations are of the highest quality with minimal risk assigned. The negative outlook indicator simply reveals that Moody’s could lower USAA’s credit rating in the long run.

However, considering that Moody’s has issued the insurer a stable outlook since 2003, a long history of stability is on USAA’s side. Still, these ratings bear watching in the years to come.

S&P Rating

S&P has a wide range of criteria with which it establishes carrier ratings, including both credit and risk factor analysis. Like the previous agencies mentioned, S&P uses a letter grade ranking system to rate each carrier.

As it stands, now, S&P has issued USAA both an Issuer Credit Rating and Financial Strength Rating of A++. Both ratings indicate the the company has a strong ability to meet its financial obligations to insurers.

More good news for present and potential insureds with USAA. Now, let’s check out another vital element that matters to consumers — customer complaints.

After all, don’t you want to know just how insureds just like yourself have fared with USAA?

Let’s dive right in.

NAIC Complaint Index

The NAIC (National Association of Insurance Commissioners) is the premier regulatory body for insurers in the United States. Take a look at the table below, revealing the most recent consumer complaint index released by the NAIC for USAA.

| Private Passenger Policies | 2016 | 2017 | 2018 |

|---|---|---|---|

| Total Complaints | 284 | 296 | 257 |

| Complaint Index (Better or Worse than National Index) | 0.57 (better) | 0.88 (better) | 0.84 (better) |

| National Complaint Index | 0.78 | 1.20 | 1.15% |

| US Market Share | 1.96% | 1.97% | 1.98% |

| Total Premiums | $4,209,032,637 | $4,559,811,404 | $4,882,340,948 |

If you glance at the table above, you’ll note that the total private passenger auto complaints that USAA received went up slightly in 2017, then dipped to its lowest level during that two-year period in 2018.

Each year, USAA’s complaint index was notably lower than the national median, not to mention the fact that their share of the U.S. insurance market rose in 2016, 2017, and 2018.

All in all, customers appear to have been very satisfied with the services USAA has to offer, as evidenced by the $673,308,311 increase in premiums written during the years noted above.

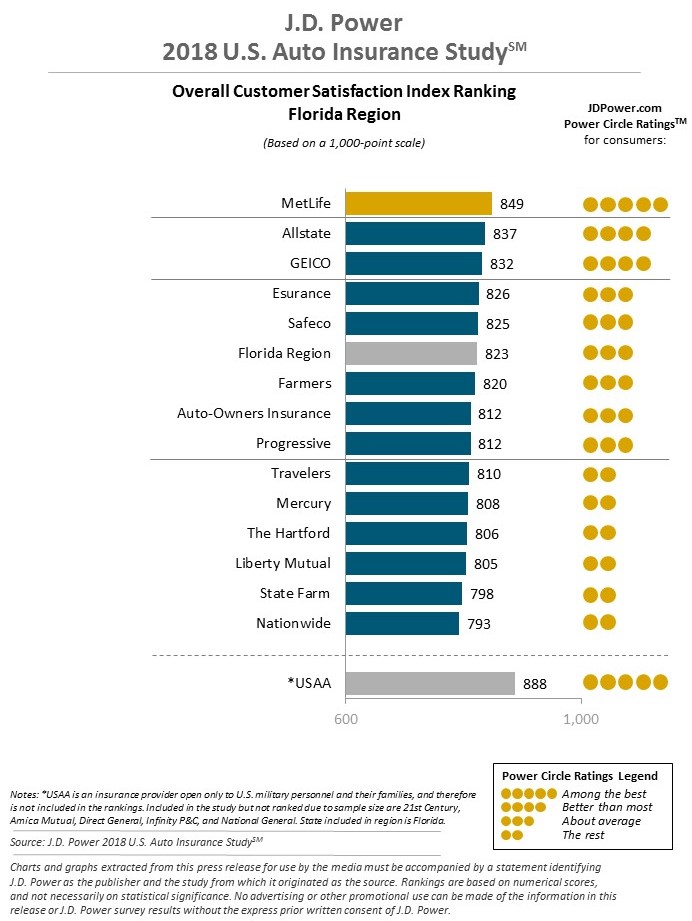

JD Power

J.D. Power’s annual insurance study revealing customer satisfaction for insureds across the country didn’t disappoint. The infographic above indicates consumer satisfaction with top insurers in the state of Florida.

Because USAA is open solely to members of the U.S. military and their families, the company was profiled but not ranked with the rest of the top carriers in J.D. Power’s study.

However, as you can see, USAA received the highest power circle rating of all the carriers listed at an astounding 888 out of 1,000 points. This makes USAA among the best in terms of customer satisfaction.

Consumer Reports

Speaking of consumer ratings, Consumer Reports is another excellent resource for current and potential insureds of USAA (or any other insurer for that matter). While a company’s financial outlook is a key piece of the decision-making puzzle, we understand that what other consumers have to say about the insurer can carry even more weight.

Check out the table below, indicating the most recent study released by Consumer Reports regarding customer satisfaction with USAA.

| Claims Process | Rating |

|---|---|

| Ease of Reaching an Agent | Excellent |

| Simplicity of the Process | Excellent |

| Promptness of Response | Excellent |

| Damage Amount | Excellent |

| Agent Courtesy | Excellent |

| Timely Payment | Excellent |

| Freedom to Select Repair Shop | Excellent |

| Being Kept Informed of Claim Status | Excellent |

The data doesn’t disappoint here either. Across, the board, USAA received excellent ratings from consumers for all aspects of the claims process from customer service to response time to payment. Based on the customer surveys that Consumer Reports gathered, USAA walked away with a 95 out of 100 consumer rating.

Consumer Affairs

After all these top scores, you might think that Consumer Affairs would follow suit — but not so. In fact, at the time this guide was written, USAA had just a 1.5-star rating based on 262 ratings submitted in the year prior.

It is worth noting that these star ratings do not include ratings outside of the prior one-year period, which means just 262 reviews were used to assign ratings out of the total 1,764 reviews. Also, USAA doesn’t currently participate in the ConsumerAffairs accreditation program, which could help explain the gap in positive ratings from the agencies previously noted.

Some of the major advantages of USAA coverage that ConsumerAffairs noted included the affordable rates, vehicle storage discount for military personnel, and stellar financial strength and claims services.

The primary disadvantages, according to ConsumerAffairs, are the fact that some discounts are not available in certain states and that insurance is available only to USAA members and their family.

FREE Car Insurance Comparison

Compare quotes from the top car insurance companies and save!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

USAA Company History

Are you ready to dig deep into USAA’s company history in this next part of our USAA auto insurance review? From the company’s share of the U.S. insurance market in recent years to its services to the carrier’s future outlook — these are all key facts to know before you decide if a carrier is right for you.

Without further ado, let’s take a closer look.

Market Share

The higher the share a company has of the insurance market, the more competitive place they hold against other insurers.

| Year | Market Share |

|---|---|

| 2015 | 4.81 % |

| 2016 | 5.04 % |

| 2017 | 5.68 % |

| 2018 | 5.87% |

While USAA’s share of the U.S. insurance market isn’t significant (partially due to the fact that they offer coverage for a very specific sector of the consumer base), their market share rose steadily for a total of 1.06 percent in the years between 2015 and 2018.

Service Options

USAA offers a wide range of online services for their products on their website, from reporting an auto claim to requesting roadside assistance. You can contact the USAA main number at 800-531-8722 with any questions and for individual services such as the Auto and Property Insurance Division.

You can also call the toll free number noted above to speak with a local agent, either by following the prompts or requesting operator assistance.

Commercials

USAA’s services are clearly geared towards a specific sector of insurance consumers — and the company’s marketing platform is no different.

With poignant messages about honor, service, and the importance of family, USAA’s commercials for their wide range of financial service products drive their core message home without getting lost in a mass of consumerism.

The commercial below emphasizes the point that USAA insurance isn’t just a coverage choice — it’s a decision that could impact the insured’s family for generations to come.

This commercial follows suit, following the story of one USAA member who’s been with the insurer his entire life with membership passed down from his father, who previously served in the U.S. Navy.

Community Service

When it comes to serving in its local communities around the country, USAA definitely doesn’t disappoint. The insurer has a strong sense of corporate responsibility, as evidenced by the multiple organizations and communities the company supports.

USAA’s signature cause is military family residency. According to the insurer’s website:

“The military lifestyle comes with unique joys, triumphs and challenges—and requires resiliency. The intent of our philanthropic investments at the national level is to make a positive impact in the lives of service members and their families by supporting programs that help them weather the challenges of military life.”

USAA supports a wide range of programs offering specific services to families of wounded, ill, injured, and fallen members of the military. The company also maintains a dedication to helping military families make sound financial decisions and providing job opportunities for former service members and their spouses.

USAA’s charitable outlook doesn’t neglect local communities by any means, with their outreach programs and financial support extending to families in need around the country. USAA also invests in educational programs that offer educators the resources they need and assist students in making sound financial choices from an early age.

Another component of USAA’s educational program outreach is to stimulate students’ interest and development in key areas of study such as science, engineering, technology, and STEM math skills in order to equip today’s youth with the vital skills they’ll need in the future.

The USAA Educational Foundation is a nonprofit entity sponsored by the insurer with the purpose to increase financial preparedness in both military and local communities around the country. The Foundation’s resources are accessible online and completely free to use.

How Is USAA Positioned for the Future?

After diving deep into various ratings and key aspects of this insurer in our USAA auto insurance review, it’s clear that this company is doing exceptionally well and is likely to retain that stance moving forward.

USAA’s overall low complaint ratio and excellent ratings by top agencies like AM Best and S&P are no small feat and its steady market share increase is also a great sign.

Consumer Affairs’ customer ratings were not nearly as favorable as what J.D. Power and Consumer Reports’ studies showed. However, the star rankings released by Consumer Affairs only included ratings from the year prior, comprising only a small fraction of the total reviews. As such, the star ratings were not a comprehensive indication of consumer satisfaction.

In addition, despite the fact that Moody’s changed USAA’s outlook from stable to negative in December 2018, this isn’t necessarily a cause for alarm. It just means that Moody’s could lower USAA’s rating in the future.

When you consider the fact that the agency still assigned USAA a stellar Aaa rating and that Moody’s has predicted a stable outlook for the insurer for well over a decade, things are still looking up for this insurer.

Assuming the company continues to offer affordable rates to consumers, fulfill their financial obligations, and provide stellar customer service, the future looks good for USAA.

Employees

https://www.youtube.com/watch?v=MxcLPag7PwY

According to Great Place to Work, 89 percent of USAA employees voted the company as a great place to work at. With approximately 33,786 employees in total, the numbers say it all. The employee population at USAA is comprised of 41 percent Millenials and 42 percent Gen Xers.

Roughly 17 percent of the employee population at USAA are Baby Boomers. Approximately 27 percent of USAA employees have worked at the company for less than two years, while 28 percent of the employee population has been employed by the insurer for between two and five years.

Just 15 percent of the USAA worker population has worked at the company for 6-10 years, while 12 percent have worked for the insurer for anywhere from 11-15 years. A minute seven percent of workers have been employed by USAA for 16-20 years. As for employees with a more than 20-year tenure at the company, roughly 11 percent of workers fall into this category.

https://www.youtube.com/watch?v=o-PQsu63rzM

Check out these interesting stats released by Great Place to Work regarding the overall employee experience of USAA workers.

- 96 percent of employees said that when you join the company you are made to feel welcome

- 95 percent of employees said they felt good about the way the company contributes to the community

- 93 percent of employees said they were proud to tell others they worked at USAA

- 92 percent of employees felt that their facilities contributed to a good working environment

- 92 percent of employees reported have special and unique benefits with the company

In 2019, USAA ranked #17 among Great Place to Work’s the Best Workplaces in Financial Services & Insurance™. Great Place to Work also ranked USAA as #47 of the Best Workplaces in Texas™ and #75 among the Best Workplaces for Millenials™ that year

USAA was also ranked #30 in 2019 Fortune 100 Best Companies to Work For® and won the eighth place in People 2019 Companies that Care®.

USAA has a 3.6-star rating on Glassdoor, based on over 2.8k reviews. Of the respondents, 64 percent state that they would recommend the company to a friend and 73 percent reported that they approved of the CEO. According to Glassdoor, USAA ranked #36 of the Best Places to Work in 2009, #22 on the Top CEOs list in 2014, and #72 on the Best Places to Interview rankings.

Over 3,000 employees have shared their salaries on Glassdoor. Financial advisors earn an average of $57,055 annually, while Financial Foundations Associates earn around the $36,893 a year mark.

https://www.youtube.com/watch?v=yy0XlnYi6Ww

Interested in joining the USAA family? Click here to visit the company’s career page and check out potential opportunities.

Cheap Car Insurance Rates

All these facts and figures are great — but we know that the rates a carrier offers could be among the top (if not the number one) components you take into account when deciding if an insurer is right for you.

USAA Availability and Rates by State

USAA is available in all 50 states. The table below indicates the average rates USAA offers in all 50 states as compared to the state average rate for all other companies. Use the search bar to see where your state hits.

| State | State Average Rate - All Companies | USAA Average Annual Rate | Higher/Lower Than State Average | Higher/Lower Percent Than State Average |

|---|---|---|---|---|

| Alaska | $3,421.51 | $2,454.21 | -$967.31 | -28.27% |

| Alabama | $3,566.96 | $2,124.09 | -$1,442.87 | -40.45% |

| Arkansas | $4,124.98 | $2,171.06 | -$1,953.92 | -47.37% |

| Arizona | $3,770.97 | $3,084.29 | -$686.68 | -18.21% |

| California | $3,688.93 | $2,693.87 | -$995.06 | -26.97% |

| Colorado | $3,876.39 | $3,338.87 | -$537.52 | -13.87% |

| Connecticut | $4,618.92 | $3,190.00 | -$1,428.92 | -30.94% |

| District of Columbia | $4,439.24 | $2,580.44 | -$1,858.80 | -41.87% |

| Delaware | $5,986.32 | $2,325.98 | -$3,660.34 | -61.15% |

| Florida | $4,680.46 | $2,850.41 | -$1,830.05 | -39.10% |

| Georgia | $4,966.83 | $3,157.46 | -$1,809.37 | -36.43% |

| Hawaii | $2,555.64 | $1,189.35 | -$1,366.29 | -53.46% |

| Iowa | $2,981.28 | $1,852.57 | -$1,128.71 | -37.86% |

| Idaho | $2,979.09 | $1,877.61 | -$1,101.48 | -36.97% |

| Illinois | $3,305.48 | $2,770.21 | -$535.28 | -16.19% |

| Indiana | $3,414.97 | $1,630.86 | -$1,784.11 | -52.24% |

| Kansas | $3,279.62 | $2,382.61 | -$897.02 | -27.35% |

| Kentucky | $5,195.40 | $2,897.89 | -$2,297.51 | -44.22% |

| Louisiana | $5,711.34 | $4,353.12 | -$1,358.23 | -23.78% |

| Maine | $2,953.28 | $1,930.79 | -$1,022.49 | -34.62% |

| Maryland | $4,582.70 | $2,744.14 | -$1,838.56 | -40.12% |

| Massachusetts | $2,678.85 | $1,458.99 | -$1,219.86 | -45.54% |

| Michigan | $10,498.64 | $3,620.00 | -$6,878.64 | -65.52% |

| Minnesota | $4,403.25 | $2,861.60 | -$1,541.65 | -35.01% |

| Missouri | $3,328.93 | $2,525.78 | -$803.15 | -24.13% |

| Mississippi | $3,664.57 | $2,056.13 | -$1,608.44 | -43.89% |

| Montana | $3,220.84 | $2,031.89 | -$1,188.96 | -36.91% |

| North Carolina | $3,393.11 | Data Not Available | ||

| North Dakota | $4,165.84 | $2,006.80 | -$2,159.04 | -51.83% |

| Nebraska | $3,283.68 | $2,330.78 | -$952.90 | -29.02% |

| New Hampshire | $3,151.77 | $1,906.96 | -$1,244.81 | -39.50% |

| New Jersey | $5,515.21 | Data Not Available | ||

| New Mexico | $3,463.64 | $2,296.77 | -$1,166.87 | -33.69% |

| Nevada | $4,861.70 | $3,069.07 | -$1,792.64 | -36.87% |

| New York | $4,289.88 | $3,761.69 | -$528.20 | -12.31% |

| Ohio | $2,709.71 | $1,478.46 | -$1,231.25 | -45.44% |

| Oklahoma | $4,142.33 | $3,174.15 | -$968.17 | -23.37% |

| Oregon | $3,467.77 | $2,587.15 | -$880.62 | -25.39% |

| Pennsylvania | $4,034.50 | $1,793.37 | -$2,241.13 | -55.55% |

| Rhode Island | $5,003.36 | $4,323.98 | -$679.38 | -13.58% |

| South Carolina | $3,781.14 | $3,424.77 | -$356.37 | -9.42% |

| South Dakota | $3,982.27 | Data Not Available | ||

| Tennessee | $3,660.89 | $2,739.28 | -$921.61 | -25.17% |

| Texas | $4,043.28 | $2,487.89 | -$1,555.39 | -38.47% |

| Utah | $3,611.89 | $2,491.10 | -$1,120.79 | -31.03% |

| Virginia | $2,357.87 | $1,858.38 | -$499.49 | -21.18% |

| Vermont | $3,234.13 | $1,903.55 | -$1,330.58 | -41.14% |

| Washington | $3,059.32 | $2,262.16 | -$797.16 | -26.06% |

| West Virginia | $2,595.36 | $1,984.62 | -$610.74 | -23.53% |

| Wisconsin | $3,606.06 | $2,975.74 | -$630.33 | -17.48% |

| Wyoming | $3,200.08 | $2,779.53 | -$420.55 | -13.14% |

| Median | $3,660.89 | $2,489.49 | -$1,171.40 | -32.00% |

You may have already noticed from the data listed above, that USAA’s rates are anywhere from roughly 9-66 percent lower than the average for each state. That’s hardly small change we’re talking about.

Comparing the Top 10 Companies by Market Share

The table below compares the average annual rates for the top-10 insurance companies across the nation, in terms of their share of the U.S. insurance market.

| State | Average by State | Allstate | American Family | Farmers | Geico | Liberty Mutual | Nationwide | Progressive | State Farm | Travelers | USAA |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Alaska | $3,421.51 | $3,145.31 | $4,153.07 | Data Not Available | $2,879.96 | $5,295.55 | Data Not Available | $3,062.85 | $2,228.12 | Data Not Available | $2,454.21 |

| Alabama | $3,566.96 | $3,311.52 | Data Not Available | $4,185.80 | $2,866.60 | $4,005.48 | $2,662.66 | $4,450.52 | $4,798.15 | $3,697.80 | $2,124.09 |

| Arkansas | $4,124.98 | $5,150.03 | Data Not Available | $4,257.87 | $3,484.63 | Data Not Available | $3,861.79 | $5,312.09 | $2,789.03 | $5,973.33 | $2,171.06 |

| Arizona | $3,770.97 | $4,904.10 | Data Not Available | $5,000.08 | $2,264.71 | Data Not Available | $3,496.08 | $3,577.50 | $4,756.25 | $3,084.74 | $3,084.29 |

| California | $3,688.93 | $4,532.96 | Data Not Available | $4,998.78 | $2,885.65 | $3,034.42 | $4,653.19 | $2,849.67 | $4,202.28 | $3,349.54 | $2,693.87 |

| Colorado | $3,876.39 | $5,537.17 | $3,733.02 | $5,290.24 | $3,091.69 | $2,797.74 | $3,739.47 | $4,231.92 | $3,270.77 | Data Not Available | $3,338.87 |

| Connecticut | $4,618.92 | $5,831.60 | Data Not Available | Data Not Available | $3,073.66 | $7,282.87 | $3,672.34 | $4,920.35 | $2,976.24 | $6,004.29 | $3,190.00 |

| District of Columbia | $4,439.24 | $6,468.92 | Data Not Available | Data Not Available | $3,692.81 | Data Not Available | $4,848.98 | $4,970.26 | $4,074.05 | Data Not Available | $2,580.44 |

| Delaware | $5,986.32 | $6,316.06 | Data Not Available | Data Not Available | $3,727.29 | $18,360.02 | $4,330.21 | $4,181.83 | $4,466.85 | $4,182.36 | $2,325.98 |

| Florida | $4,680.46 | $7,440.46 | Data Not Available | Data Not Available | $3,783.63 | $5,368.15 | $4,339.60 | $5,583.30 | $3,397.67 | Data Not Available | $2,850.41 |

| Georgia | $4,966.83 | $4,210.70 | Data Not Available | Data Not Available | $2,977.20 | $10,053.44 | $6,484.90 | $4,499.22 | $3,384.88 | Data Not Available | $3,157.46 |

| Hawaii | $2,555.64 | $2,173.49 | Data Not Available | $4,763.82 | $3,358.86 | $3,189.55 | $2,551.83 | $2,177.93 | $1,040.28 | Data Not Available | $1,189.35 |

| Iowa | $2,981.28 | $2,965.86 | $3,021.81 | $2,435.72 | $2,296.16 | $4,415.28 | $2,735.44 | $2,395.50 | $2,224.51 | $5,429.38 | $1,852.57 |

| Idaho | $2,979.09 | $4,088.76 | $3,728.79 | $3,168.28 | $2,770.68 | $2,301.51 | $3,032.19 | Data Not Available | $1,867.96 | $3,226.29 | $1,877.61 |

| Illinois | $3,305.48 | $5,204.41 | $3,815.31 | $4,605.20 | $2,779.16 | $2,277.65 | $2,711.81 | $3,536.65 | $2,344.88 | $2,499.76 | $2,770.21 |

| Indiana | $3,414.97 | $3,978.81 | $3,679.68 | $3,437.55 | $2,261.07 | $5,781.35 | Data Not Available | $3,898.00 | $2,408.94 | $3,393.75 | $1,630.86 |

| Kansas | $3,279.62 | $4,010.23 | $2,146.40 | $3,703.77 | $3,220.65 | $4,784.42 | $2,475.59 | $4,144.38 | $2,720.00 | $4,341.43 | $2,382.61 |

| Kentucky | $5,195.40 | $7,143.92 | Data Not Available | Data Not Available | $4,633.59 | $5,930.97 | $5,503.23 | $5,547.63 | $3,354.32 | $6,551.68 | $2,897.89 |

| Louisiana | $5,711.34 | $5,998.79 | Data Not Available | Data Not Available | $6,154.60 | Data Not Available | Data Not Available | $7,471.10 | $4,579.12 | Data Not Available | $4,353.12 |

| Maine | $2,953.28 | $3,675.59 | Data Not Available | $2,770.15 | $2,823.05 | $4,331.39 | Data Not Available | $3,643.59 | $2,198.68 | $2,252.97 | $1,930.79 |

| Maryland | $4,582.70 | $5,233.17 | Data Not Available | Data Not Available | $3,832.63 | $9,297.55 | $2,915.69 | $4,094.86 | $3,960.87 | Data Not Available | $2,744.14 |

| Massachusetts | $2,678.85 | $2,708.53 | Data Not Available | Data Not Available | $1,510.17 | $4,339.35 | Data Not Available | $3,835.11 | $1,361.86 | $3,537.94 | $1,458.99 |

| Michigan | $10,498.64 | $22,902.59 | Data Not Available | $8,503.60 | $6,430.11 | $20,000.04 | $6,327.38 | $5,364.55 | $12,565.52 | $8,773.97 | $3,620.00 |

| Minnesota | $4,403.25 | $4,532.01 | $3,521.29 | $3,137.45 | $3,498.54 | $13,563.61 | $2,926.49 | Data Not Available | $2,066.99 | Data Not Available | $2,861.60 |

| Missouri | $3,328.93 | $4,096.15 | $3,286.90 | $4,312.19 | $2,885.33 | $4,518.67 | $2,265.35 | $3,419.14 | $2,692.91 | Data Not Available | $2,525.78 |

| Mississippi | $3,664.57 | $4,942.11 | Data Not Available | Data Not Available | $4,087.21 | $4,455.94 | $2,756.53 | $4,308.85 | $2,980.48 | $3,729.32 | $2,056.13 |

| Montana | $3,220.84 | $4,672.10 | Data Not Available | $3,907.55 | $3,602.35 | $1,326.11 | $3,478.26 | $4,330.76 | $2,417.74 | Data Not Available | $2,031.89 |

| North Carolina | $3,393.11 | $7,190.43 | Data Not Available | Data Not Available | $2,936.69 | $2,182.71 | $2,848.03 | $2,382.61 | $3,078.65 | $3,132.66 | Data Not Available |

| North Dakota | $4,165.84 | $4,669.31 | $3,812.40 | $3,092.49 | $2,668.24 | $12,852.83 | $2,560.35 | $3,623.06 | $2,560.53 | Data Not Available | $2,006.80 |

| Nebraska | $3,283.68 | $3,198.83 | $2,215.13 | $3,997.29 | $3,837.49 | $6,241.52 | $2,603.94 | $3,758.01 | $2,438.71 | Data Not Available | $2,330.78 |

| New Hampshire | $3,151.77 | $2,725.01 | Data Not Available | Data Not Available | $1,615.02 | $8,444.41 | $2,491.10 | $2,694.45 | $2,185.46 | Data Not Available | $1,906.96 |

| New Jersey | $5,515.21 | $5,713.58 | Data Not Available | $7,617.00 | $2,754.94 | $6,766.62 | Data Not Available | $3,972.72 | $7,527.16 | $4,254.49 | Data Not Available |

| New Mexico | $3,463.64 | $4,200.65 | Data Not Available | $4,315.53 | $4,458.30 | Data Not Available | $3,514.38 | $3,119.18 | $2,340.66 | Data Not Available | $2,296.77 |

| Nevada | $4,861.70 | $5,371.62 | $5,441.18 | $5,595.56 | $3,662.09 | $6,201.55 | $3,477.14 | $4,062.57 | $5,796.34 | $5,360.41 | $3,069.07 |

| New York | $4,289.88 | $4,740.97 | Data Not Available | Data Not Available | $2,428.24 | $6,540.73 | $4,012.93 | $3,771.15 | $4,484.58 | $4,578.79 | $3,761.69 |

| Ohio | $2,709.71 | $3,197.22 | $1,515.17 | $3,423.01 | $1,867.19 | $4,429.74 | $3,300.89 | $3,436.96 | $2,507.88 | $3,135.16 | $1,478.46 |

| Oklahoma | $4,142.33 | $3,718.62 | Data Not Available | $4,142.40 | $3,437.34 | $6,874.62 | Data Not Available | $4,832.35 | $2,816.80 | Data Not Available | $3,174.15 |

| Oregon | $3,467.77 | $4,765.95 | $3,527.28 | $3,753.52 | $3,220.12 | $4,334.55 | $3,176.83 | $3,629.13 | $2,731.48 | $2,892.19 | $2,587.15 |

| Pennsylvania | $4,034.50 | $3,984.12 | Data Not Available | Data Not Available | $2,605.22 | $6,055.20 | $2,800.37 | $4,451.00 | $2,744.23 | $7,842.47 | $1,793.37 |

| Rhode Island | $5,003.36 | $4,959.45 | Data Not Available | Data Not Available | $5,602.63 | $6,184.12 | $4,409.63 | $5,231.09 | $2,406.51 | $6,909.45 | $4,323.98 |

| South Carolina | $3,781.14 | $3,903.43 | Data Not Available | $4,691.85 | $3,178.01 | Data Not Available | $3,625.49 | $4,573.08 | $3,071.34 | Data Not Available | $3,424.77 |

| South Dakota | $3,982.27 | $4,723.72 | $4,047.47 | $3,768.80 | $2,940.29 | $7,515.99 | $2,737.66 | $3,752.81 | $2,306.23 | Data Not Available | Data Not Available |

| Tennessee | $3,660.89 | $4,828.85 | Data Not Available | $3,430.07 | $3,283.42 | $6,206.69 | $3,424.96 | $3,656.91 | $2,639.30 | $2,738.52 | $2,739.28 |

| Texas | $4,043.28 | $5,485.44 | $4,848.72 | Data Not Available | $3,263.28 | Data Not Available | $3,867.55 | $4,664.69 | $2,879.94 | Data Not Available | $2,487.89 |

| Utah | $3,611.89 | $3,566.42 | $3,698.77 | $3,907.99 | $2,965.57 | $4,327.76 | $2,986.57 | $3,830.10 | $4,645.83 | Data Not Available | $2,491.10 |

| Virginia | $2,357.87 | $3,386.80 | Data Not Available | Data Not Available | $2,061.53 | Data Not Available | $2,073.00 | $2,498.58 | $2,268.95 | Data Not Available | $1,858.38 |

| Vermont | $3,234.13 | $3,190.38 | Data Not Available | Data Not Available | $2,195.71 | $3,621.08 | $2,128.21 | $5,217.14 | $4,382.84 | Data Not Available | $1,903.55 |

| Washington | $3,059.32 | $3,540.52 | $3,713.02 | $2,962.00 | $2,568.65 | $3,994.73 | $2,129.84 | $3,209.52 | $2,499.78 | Data Not Available | $2,262.16 |

| West Virginia | $2,595.36 | $3,820.68 | Data Not Available | Data Not Available | $2,120.80 | $2,924.39 | Data Not Available | Data Not Available | $2,126.32 | Data Not Available | $1,984.62 |

| Wisconsin | $3,606.06 | $4,854.41 | $1,513.27 | $3,777.49 | $3,926.20 | $6,758.85 | $5,224.99 | $3,128.91 | $2,387.53 | Data Not Available | $2,975.74 |

| Wyoming | $3,200.08 | $4,373.93 | Data Not Available | $3,069.35 | $3,496.56 | $1,989.36 | $3,187.20 | $4,401.17 | $2,303.55 | Data Not Available | $2,779.53 |

| Median | $3,660.89 | $4,532.96 | $3,698.77 | $3,907.99 | $3,073.66 | $5,295.55 | $3,187.20 | $3,935.36 | $2,731.48 | $3,729.32 | $2,489.49 |

If you take the rates for the other top nine providers in the state of Florida, for instance, you’ll notice that USAA’s rates are by far the cheapest of the carriers listed where data is available.

Case in point, Allstate charges insureds an average of $7,440.46 for coverage, while USAA comes in at just $2,850.41 in annual premiums. That’s an approximate $4,600 difference in rates between these two insurers.

Average Annual USAA Male vs. Female Car Insurance Rates

The table below indicates the average annual rates of different carriers, including USAA, charge consumers based on their gender.

| Group | Married 35-year old female | Married 35-year old male | Married 60-year old female | Married 60-year old male | Single 17-year old female | Single 17-year old male | Single 25-year old female | Single 25-year old male |

|---|---|---|---|---|---|---|---|---|

| Allstate | $3,156.09 | $3,123.01 | $2,913.37 | $2,990.64 | $9,282.19 | $10,642.53 | $3,424.87 | $3,570.93 |

| American Family | $2,202.70 | $2,224.31 | $1,992.92 | $2,014.38 | $5,996.50 | $8,130.50 | $2,288.65 | $2,694.72 |

| Farmers | $2,556.98 | $2,557.75 | $2,336.80 | $2,448.39 | $8,521.97 | $9,144.04 | $2,946.80 | $3,041.44 |

| Geico | $2,302.89 | $2,312.38 | $2,240.60 | $2,283.45 | $5,653.55 | $6,278.96 | $2,378.89 | $2,262.87 |

| Liberty Mutual | $3,802.77 | $3,856.84 | $3,445.00 | $3,680.53 | $11,621.01 | $13,718.69 | $3,959.67 | $4,503.13 |

| Nationwide | $2,360.49 | $2,387.43 | $2,130.26 | $2,214.62 | $5,756.37 | $7,175.31 | $2,686.48 | $2,889.04 |

| Progressive | $2,296.90 | $2,175.27 | $1,991.49 | $2,048.63 | $8,689.95 | $9,625.49 | $2,697.73 | $2,758.66 |

| State Farm | $2,081.72 | $2,081.72 | $1,873.89 | $1,873.89 | $5,953.88 | $7,324.34 | $2,335.96 | $2,554.56 |

| Travelers | $2,178.66 | $2,199.51 | $2,051.98 | $2,074.41 | $9,307.32 | $12,850.91 | $2,325.25 | $2,491.21 |

| USAA | $1,551.43 | $1,540.32 | $1,449.85 | $1,448.98 | $4,807.54 | $5,385.61 | $1,988.52 | $2,126.14 |

For each age and gender demographics, USAA charges by far the cheapest rates of all the carriers listed. For example, while a carrier such as Farmers charges $9,144.04 annually to single, 17-year-old male drivers, USAA’s rates are just $5,385.61 to the same demographic.

Average Annual USAA Commute Rates

| Group | 10 miles commute. 6000 annual mileage. | 25 miles commute. 12000 annual mileage. |

|---|---|---|

| Allstate | $4,841.71 | $4,934.20 |

| American Family | $3,401.30 | $3,484.88 |

| Farmers | $4,179.32 | $4,209.22 |

| Geico | $3,162.64 | $3,267.37 |

| Liberty Mutual | $5,995.27 | $6,151.63 |

| Nationwide | $3,437.33 | $3,462.67 |

| Progressive | $4,030.02 | $4,041.01 |

| State Farm | $3,175.98 | $3,344.01 |

| Travelers | $4,399.85 | $4,469.96 |

| USAA | $2,482.69 | $2,591.91 |

Did you know that some carriers will charge you higher annual premiums based on the length of your commute? Depending on the company you choose, some carriers will charge you the exact same rate and others show a notable difference in premiums if you have a longer commute time.

USAA is one of the companies that will charge you higher rates if you have a longer commute to work each day. In fact, the company charges consumers with a 25-mile commute to work each day roughly $100 more a year than insureds with a 10-mile commute to work.

With that said, the company’s commute rates are still by far the cheapest of all the carriers listed.

Average Annual USAA Rates by Vehicle Make and Model

Your vehicle’s make and model will also impact the rates you pay. Check out the table below, to see how your rates could fluctuate based on your car and the carrier you pick.

| Make and Model | USAA | Geico | State Farm | American Family | Nationwide | Progressive | Farmers | Travelers | Allstate | Liberty Mutual | Grand Total |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2015 Ford F-150 Lariat SuperCab with 2WD 6.5 foot bed and 2.7L V6 | $2,551.56 | $3,092.11 | $3,204.23 | $3,447.30 | $3,571.01 | $3,914.05 | $4,093.50 | $4,023.47 | $4,429.74 | $5,830.16 | $3,791.74 |

| 2015 Honda Civic Sedan LX with 2.0L 4cyl and CVT | $2,409.67 | $3,092.58 | $3,024.24 | $3,178.82 | $3,547.84 | $4,429.56 | $4,405.21 | $4,420.37 | $4,753.69 | $5,869.32 | $3,890.45 |

| 2015 Toyota RAV4 XLE | $2,454.58 | $3,090.89 | $3,226.02 | $3,326.18 | $3,517.03 | $3,647.22 | $3,728.22 | $4,383.78 | $4,324.99 | $5,825.33 | $3,721.25 |

| 2018 Ford F-150 Lariat SuperCab with 2WD 6.5 foot bed and 2.7L V6 | $2,855.69 | $3,338.40 | $3,497.17 | $3,487.91 | $3,373.64 | $3,962.58 | $4,390.19 | $4,412.42 | $5,491.12 | $5,988.85 | $4,076.10 |

| 2018 Honda Civic Sedan LX with 2.0L 4cyl and CVT | $2,422.66 | $3,338.87 | $3,189.99 | $3,721.32 | $3,361.93 | $4,528.90 | $4,779.51 | $4,661.22 | $5,380.28 | $6,682.63 | $4,166.72 |

| 2018 Toyota RAV4 XLE | $2,529.63 | $3,337.18 | $3,418.33 | $3,496.99 | $3,328.57 | $3,730.78 | $3,769.00 | $4,708.19 | $4,947.90 | $6,244.44 | $3,926.83 |

The table above lists out the average annual rates that different carriers, including USAA, charge based on the type of vehicle the insured owns, along with the grand total average for each company. Yet again, USAA charges the cheapest rates for each vehicle make and model of all the carriers listed.

For example, if you look at what Liberty Mutual charges customers who own a 2015 Toyota RAV4

XLE vs. what USAA charges insureds with the same vehicle, you’ll see that there is an approximate $3,400 difference in rates between these two carriers.

Average Annual USAA Coverage Level Rates

| Group | High | Low | Medium |

|---|---|---|---|

| Allstate | $5,139.02 | $4,628.03 | $4,896.81 |

| American Family | $3,416.40 | $3,368.49 | $3,544.37 |

| Farmers | $4,494.13 | $3,922.47 | $4,166.22 |

| Geico | $3,429.14 | $3,001.91 | $3,213.97 |

| Liberty Mutual | $6,356.04 | $5,805.75 | $6,058.57 |

| Nationwide | $3,505.37 | $3,394.83 | $3,449.80 |

| Progressive | $4,350.96 | $3,737.13 | $4,018.46 |

| State Farm | $3,454.80 | $3,055.40 | $3,269.80 |

| Travelers | $4,619.07 | $4,223.63 | $4,462.02 |

| USAA | $2,667.92 | $2,404.11 | $2,539.87 |

The table we have here indicates the average rates USAA charges based on the coverage level you pick as compared to the other top nine carriers across the nation. As you were likely expecting by now — yes, USAA comes in again with the cheapest rates of all the carriers listed.

In fact, USAA charges consumers who pick high. vs low levels of coverage just $263 more per year in annual premiums. If you compare that rate gap to another carrier like Allstate, you’ll see that the company charges insureds who pick high coverage levels about $500 more per year than individuals who opt for low levels of coverage.

Average Annual USAA Credit History Rates

| Group | Fair | Good | Poor |

|---|---|---|---|

| Allstate | $4,581.16 | $3,859.66 | $6,490.65 |

| American Family | $3,169.53 | $2,691.74 | $4,467.98 |

| Farmers | $3,899.41 | $3,677.12 | $4,864.14 |

| Geico | $2,986.79 | $2,434.82 | $4,259.50 |

| Liberty Mutual | $5,604.24 | $4,388.18 | $8,802.22 |

| Nationwide | $3,254.83 | $2,925.94 | $4,083.29 |

| Progressive | $3,956.31 | $3,628.85 | $4,737.64 |

| State Farm | $2,853.00 | $2,174.26 | $4,951.20 |

| Travelers | $4,344.10 | $4,058.97 | $5,160.22 |

| USAA | $2,219.83 | $1,821.20 | $3,690.73 |

Apart from a mere handful of states where the practice is illegal, insurers across the nation can and will charge you higher rates based on your credit history. The question is — how much more?

USAA actually shows a significant gap in rates for consumers with a good vs. poor credit history. They charge insureds with poor credit roughly $3,700 more per year than individuals who have good credit.

For comparison purposes, let’s look at another insurer listed in the table above to see if this rate gap is really so extreme. Surprisingly, Allstate, a carrier that has shown notably more expensive premiums based on other rate factors, charges only approximately $2,600 more a year to consumers with poor vs. good credit.

While USAA has been shown to have the cheapest rates overall of the top carriers listed, the insurer still shows a noticeable gap in rates when it comes to consumer credit history. If your credit is less than stellar though, no need to despair.

As of 2017, Experian reported that the national average credit score 675. Furthermore, their study reported that roughly 20 percent of Americans have very high credit scores.

It’s never too late to start practicing good credit habits. By paying down any existing credit card debt and committing to not spend more in the future than you can pay off in a given month, the road to improved credit (and cheaper rates!) could be just ahead.

Average Annual USAA Driving Record Rates

| Group | Clean record | With 1 accident | With 1 DUI | With 1 speeding violation |

|---|---|---|---|---|

| Allstate | $3,819.90 | $4,987.68 | $6,260.73 | $4,483.51 |

| American Family | $2,693.61 | $3,722.75 | $4,330.24 | $3,025.74 |

| Farmers | $3,460.60 | $4,518.73 | $4,718.75 | $4,079.01 |

| Geico | $2,145.96 | $3,192.77 | $4,875.87 | $2,645.43 |

| Liberty Mutual | $4,774.30 | $6,204.78 | $7,613.48 | $5,701.26 |

| Nationwide | $2,746.18 | $3,396.95 | $4,543.20 | $3,113.68 |

| Progressive | $3,393.09 | $4,777.04 | $3,969.65 | $4,002.28 |

| State Farm | $2,821.18 | $3,396.01 | $3,636.80 | $3,186.01 |

| Travelers | $3,447.69 | $4,289.74 | $5,741.40 | $4,260.80 |

| USAA | $1,933.68 | $2,516.24 | $3,506.03 | $2,193.25 |

It shouldn’t come as a shock that your driving record will impact the rates you pay for car insurance. After all, if a consumer has a history of accidents or driving violations, the individual naturally presents more of a risk to insure.

Across all categories, USAA again by far charges the cheapest rates of all the carriers listed. However, they do charge individuals with one DUI on their record roughly $1,500 more annually than insureds with a clean driving record.

While this rate gap might seem significant, it’s still notably less than the difference in rates that a carrier like Travelers charges consumers with one DUI vs. a clean driving history. In fact, Travelers charges individuals with one DUI roughly $2,300 more annually than insureds who have a clean record.

Coverages Offered by USAA

Ready to find out what coverages are available to you if you select USAA? From the primary types of coverage to key discounts you won’t want to miss — our team did the research for this USAA auto insurance review and broke down the data so you don’t have to.

Let’s jump right in!

Policy Options

Check out the following options USAA offers when you’re structuring your policy.

Liability Coverage: Liability coverage is typically comprised of two parts — bodily injury coverage and property damage coverage. Both exist to protect you and pay for damages other parties sustain in an accident for which you are found to be at fault.

Comprehensive Coverage: Comprehensive coverage will pay for damage to your vehicle caused by an incident other than rollover or crash. Things like vehicle theft, vandalism, fire, hail, and flooding are all examples of scenarios where comprehensive coverage could come into play.

Collision Coverage: Unlike comprehensive coverage that covers occurrences such a stolen vehicle, collision coverage exists to pay for any damage to your vehicle resulting from a rollover or crash. Collision coverage applies regardless of who was at fault for the collision.

Personal Injury Protection: Personal Injury Protection or PIP for short will pay for damages stemming from an auto accident that you or your passengers incur. PIP applies regardless of who caused the crash. Examples of expenses that PIP could typically cover include lost wages, medical bills, funeral costs, and disability. PIP is mandatory by law in the state of Florida, which is a no-fault state.

Extended Benefits Coverage: Extended benefits coverage provides services disability benefits and wage earner benefits. There are also death benefits. The coverage can only be applied to the policy if the insured also carries medical payments coverage.

Uninsured and Underinsured Motorist Bodily Injury Coverage: This type of coverage comes into effect to cover the costs of any injuries incurred by you and/or your passengers in a collision caused by an uninsured or hit-and-run motorist.

Uninsured and Underinsured Motorist Property Damage Coverage: If you are involved in a crash with a hit-and run-driver, this type of coverage will pay for resulting damage to your car.

Roadside Assistance: Roadside assistance coverage will help cover towing or repair costs if your car leaves you stranded or won’t start. This type of coverage also includes car unlocking, gas delivery, and tire changing services.

Rental Reimbursement: Rental reimbursement coverage will pay for rental car costs if your car is being repaired for a covered claim.

Accident Forgiveness: If you don’t get into a crash for five years while covered by USAA, then your premium won’t go up if you get into one accident where you’re the at-fault driver.

Bundles

Bundling your policies with USAA could mean you save big on multiple types of insurance. You could save up to 10 percent on your policies with USAA if you opt to bundle your property and auto insurance together.

Discounts

Who doesn’t want to save on car insurance? USAA offers a wide range of discounts to former and current military service members and their families, including vehicle garaging discounts.

Check out the table below to see how much you could save on your policy.

| Discount Type | Amount Saved |

|---|---|

| Anti-lock Brakes | Not Listed |

| Anti-Theft | Not Listed |

| Claim Free | 12% |

| Daytime Running Lights | Not Listed |

| Defensive Driver | 3% |

| Distant Student | Not Listed |

| Driver's Education | 3% |

| Driving Device/App | 5% |

| Early Signing | 12% |

| Family Legacy | 10% |

| Garaging/Storing | 90% |

| Good Student | 3% |

| Low Mileage | Not Listed |

| Loyalty | Not Listed |

| Married | Not Listed |

| Military | Not Listed |

| Military Garaging | 15% |

| Multiple Policies | Not Listed |

| Multiple Vehicles | Not Listed |

| Newer Vehicle | 12% |

| Occasion Operator | Not Listed |

| Paperless/Auto Billing | 3% |

| Passive Restraint | Not Listed |

| Safe Driver | 12% |

| Senior Driver | Not Listed |

| Vehicle Recovery | Not Listed |

| VIN Etching | Not Listed |

| Young Driver | $75 |

As you can see, you could save anywhere from 3-90 percent depending on the type of discount. You’ll also notice that some discounts don’t have exact savings listed, partially because the amount varies depending on the insured.

For example, young, 20-something drivers could save up to 10 percent with the Family Legacy Discount. Eligibility criteria include that you must be under the age of 25, have been covered on your parent’s policy for at least three years, and have a clean driving record.

Speak with your agent when structuring your policy to see what discounts you could be eligible for and just how much you could save on auto insurance.

USAA’s Rideshare Gap Coverage

USAA offers several special coverage options that consumers may want to consider taking advantage of when structuring their policy.

One such program is the company’s Ridesharing Gap Coverage. This serves to cover rideshare drivers who may not be covered by their regular policy or commercial policy when waiting for a rideshare request.

Overall, USAA has an excellent selection of discounts that could apply to a wide range of drivers.

It is also important to note that certain discounts vary in availability by state. Some safety features aren’t listed as discounts, but certain safety features almost always will help lower your rates.

This is why it’s essential to inquire with your agent when determining your coverages to make sure you don’t miss out on any potential discounts.

FREE Car Insurance Comparison

Compare quotes from the top car insurance companies and save!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Canceling Your Policy

If for some reason you are covered by USAA and find that you need to cancel your policy, you generally have three options to do so. Here’s what you need to know.

Cancellation Fee

USAA allows you to cancel your policy at any time, without having to worry about cancellation fees. You would only be required to pay a fee if you simply allowed your policy to lapse without informing the insurer.

In such scenarios, you would then be required to fulfill the policy premium and any applicable late fees.

Is there a Refund?

On top of no cancellation fees, depending on your situation, you could also qualify for a prorated refund of yet unused premiums.

How to Cancel

Before you cancel your policy, you’ll need to be prepared to provide the following:

- Your policy number and the date you wish the cancellation to go into effect

- Your full name, date of birth, address, and Social Security number

- The reason you’re canceling your policy

- The name of your new insurer and policy number, assuming you are switching insurers

As mentioned previously, you’ll have three options to cancel your policy. Thes are online, by phone, or via mail.

- To cancel online, simply log into your account (or create one) and contact a customer service agent with USAA.

- To cancel by phone, you can contact customer service at 800-531-8722 and provide the information noted above.

- Canceling by mail will take the longest amount of time.

- Besides including the reason for your cancellation, you will also need to provide your name and address, effective policy end date, your USAA policy number, and your dated signature.

- You should allow a minimum of 30 days from when you mail the letter to when you want the policy to terminate.

- You can mail the notice of cancellation to 9800 Fredricksburg Rd., San Antonio, TX, 78288.

When Can I Cancel?

You can cancel your policy at any time. There is no specific window of time set in which you are required to cancel if you feel you need to make a change to your current coverage.

How to Make a Claim

If you ever get into a crash, it’s vital to know what’s involved in reporting a claim to make the process as seamless and stress-free as possible.

Thankfully, USAA has a fast and efficient claim reporting system. Let’s take a closer look.

Ease of Making a Claim

You can report your claim either over the phone or online as you prefer. To report your claim over the phone, simply call the Claims Department at 800-531-8722.

You can also file and check the status of your claim online through your USAA account. Click here to learn more.

Premiums Written

As you know by now from the first part of our USAA auto insurance review, the company has been highly ranked by multiple rating agencies for its ability to fulfill its financial obligations to insureds.

Another excellent way to determine the financial stability of any given insurer and their ability to fulfill claims is to look at the data for their total written premiums and loss ratios.

Check out the table below, indicating the number of premiums USAA wrote between 2015 and 2018.

| Year | Premiums Written |

|---|---|

| 2015 | 10,562,100 |

| 2016 | 11,691,051 |

| 2017 | 13,154,939 |

| 2018 | 14,467,936 |

This all boils down to more good news for USAA — as you can see, the company’s direct premiums written increased steadily during this three-year period with a total jump of 3,905,836 premiums written from 2015 to 2018.

Loss Ratio

| Year | Loss Ratio |

|---|---|

| 2015 | 82.82 % |

| 2016 | 86.24 % |

| 2017 | 79.60 % |

| 2018 | 0.77% |

Loss ratio is another vital indicator when measuring a company’s financial stability and future outlook because this reveals how much the insurer is paying out in comparison to the premiums it’s earning back.

If an insurer experiences and continues to see a loss ratio over 100 percent, this means they are losing money consistently — which spells bad news all around.

USAA’s loss ratio in recent years has been within the normal, healthy range, albeit on the higher end between 2015 and 2017. The insurer’s loss ratio elevated slightly between 2015 and 2016, went down in 2017, and dropped to a negligible figure in 2018.

This reveals that USAA is paying out a solid proportion of claims out in conjunction with what the company is earning back in premiums.

How to Get a Quote Online

Now that you’ve got the inside scoop from our USAA auto insurance review, how do you go about getting your quote to see what your coverage options are?

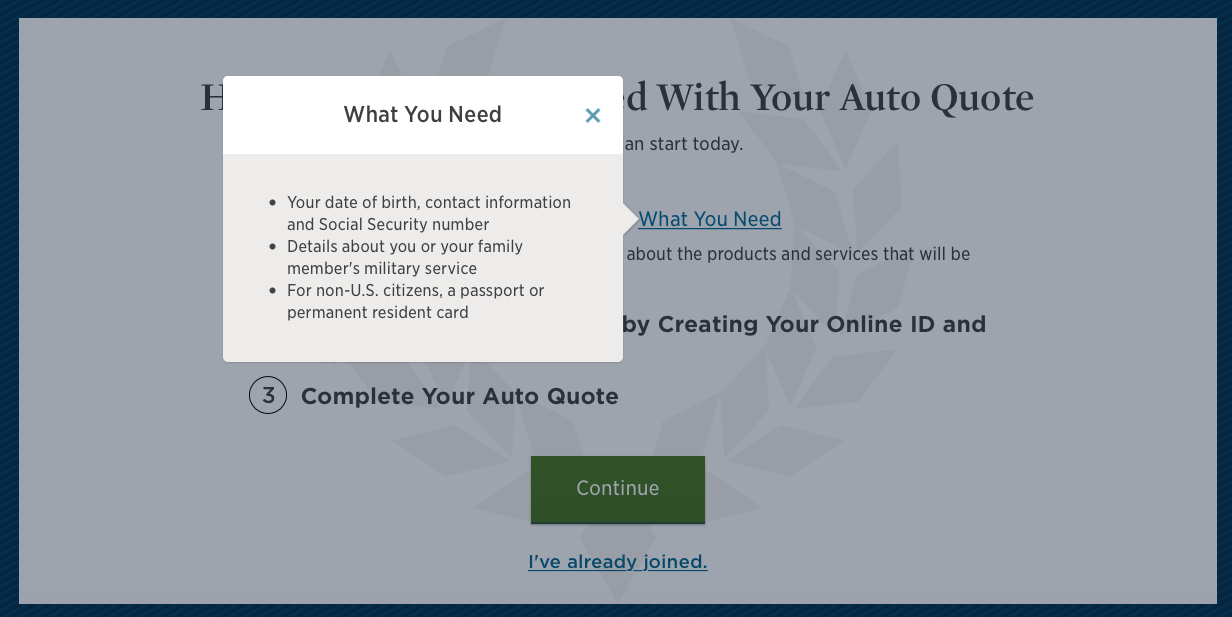

We’re so glad you asked. Before you get started, you’ll need to have the following information available:

- Date of birth

- Contact details

- Social Security number

- Information about you or a member of your family’s military service

- Your passport of U.S. resident card if you aren’t a citizen

Are you ready? Here’s your step-by-step guide to obtaining an online quote from USAA.

Navigate to the USAA Website

Start by going to USAA’s website. Then, scroll down to the middle of the page until you see the options below.

Create an Account

Once you click “Get a Free Quote”, you’ll be directed to the page above. If you don’t already have an account with USAA, you’ll need to create one. Click “Join Online”, then move to the next step.

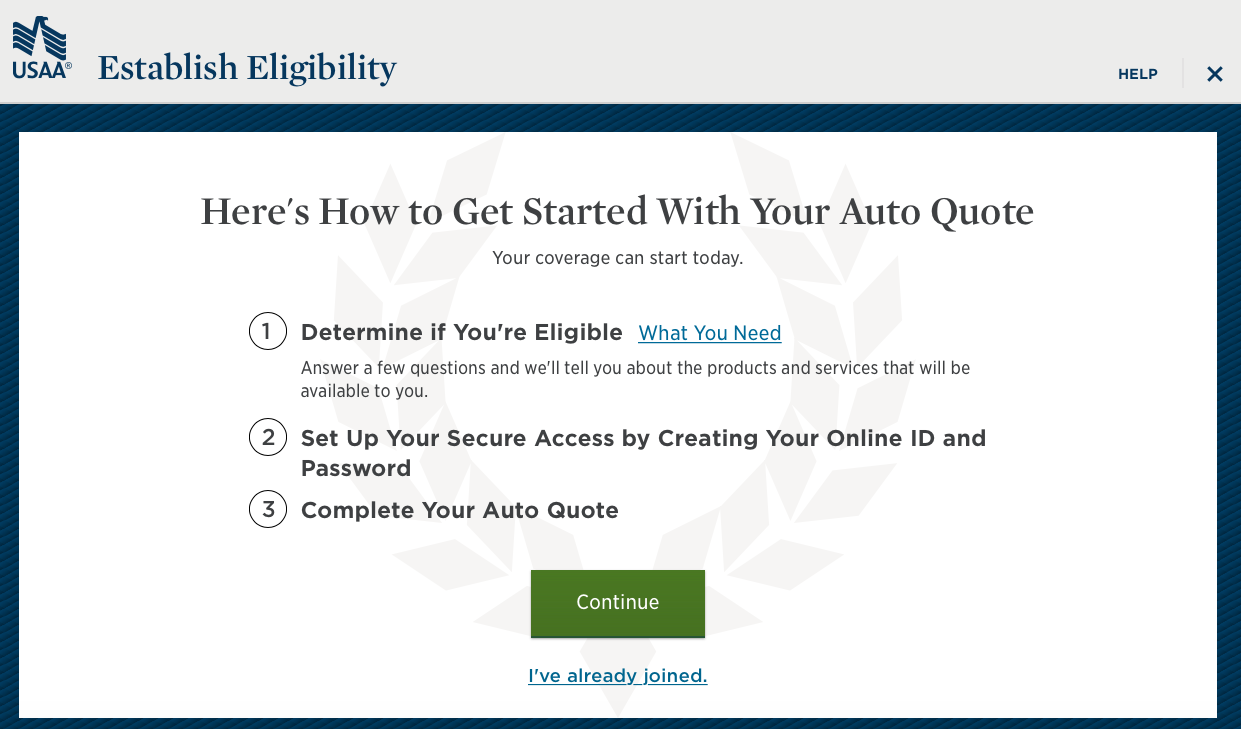

Getting Started

You will be redirected the page above, detailing the steps involved to access your quote. If you click on the “What You Need” hyperlink, you’ll see the list of items you should already have with you to access your quote.

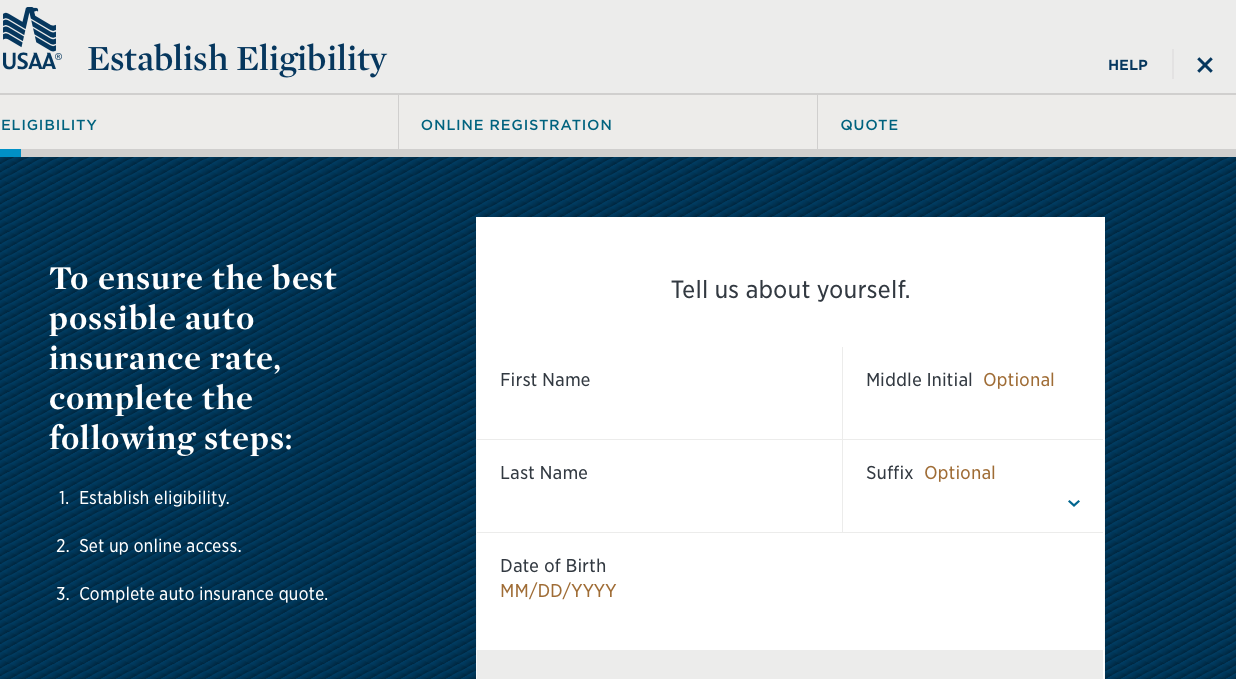

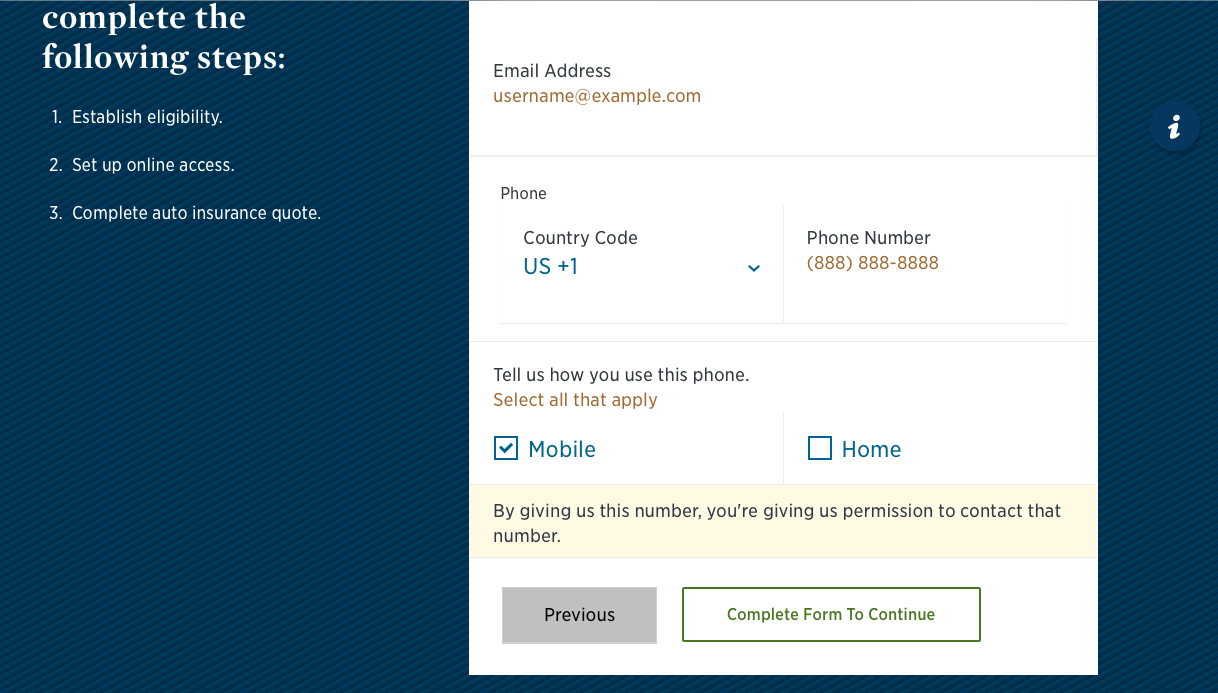

Establish Eligibility

Next, you’ll need to fill in some personal details, including your name, date of birth, email, and phone number. Once completed, click forward to the next page.

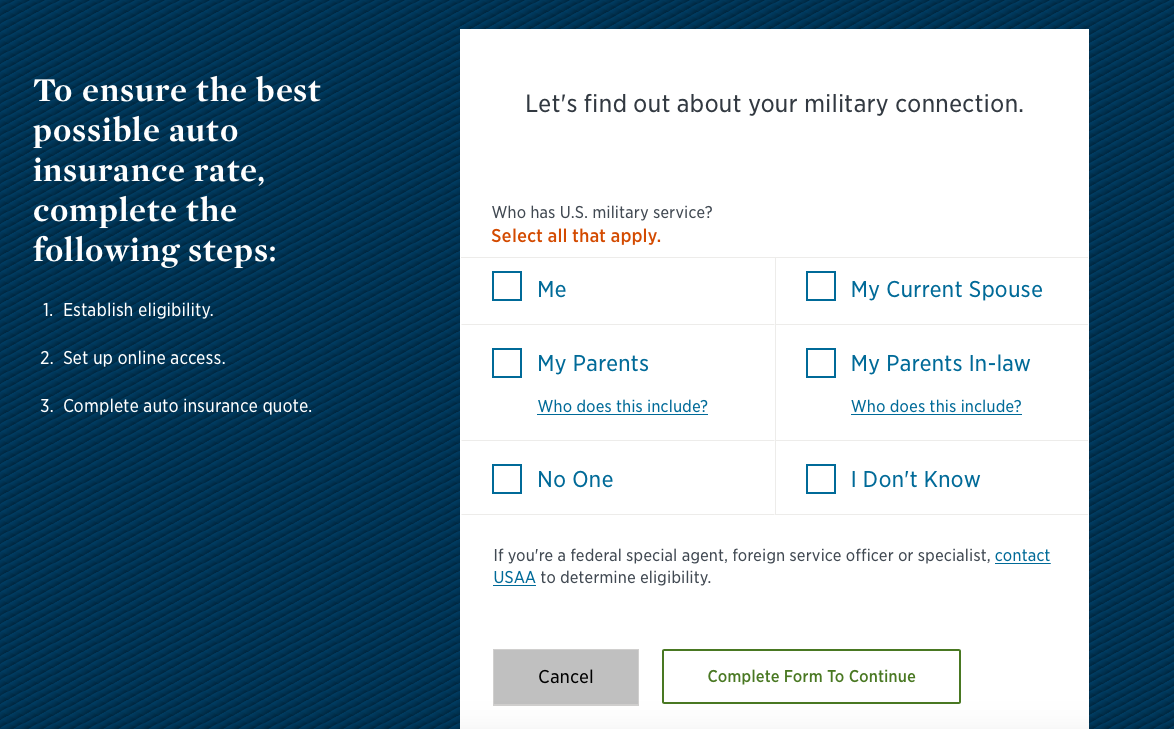

Identifying Your Military Connection

At this point, it’s time to choose what your military connection is, whether it be you or a member of your family. Check any boxes that apply to you. The boxes you select will determine what the form brings up next.

Before receiving your final quote, you’ll need to provide actual details regarding your military connection. Follow the prompts on each page and within a few minutes, you’ll have your free quote.

FREE Car Insurance Comparison

Compare quotes from the top car insurance companies and save!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Website Design

USAA’s website is very simple and easy to navigate. You’ll see the home page above, where you’ll find options to join USAA, learn more, and look at options from insurance to banking among the plethora of financial services the company offers.

If you scroll down a bit more, you’ll see the above, with contact information to reach USAA’s customer support team and information about the company’s handy mobile app (more on that in a bit).

Scrolling down towards the bottom, you’ll see easy navigation links to the wide range of services USAA offers from banking to insurance to investment portfolios.

Finally, at the very bottom of the home page, you’ll find everything you need to contact the customer support team, claims center, request roadside assistance, learn about career opportunities, and more.

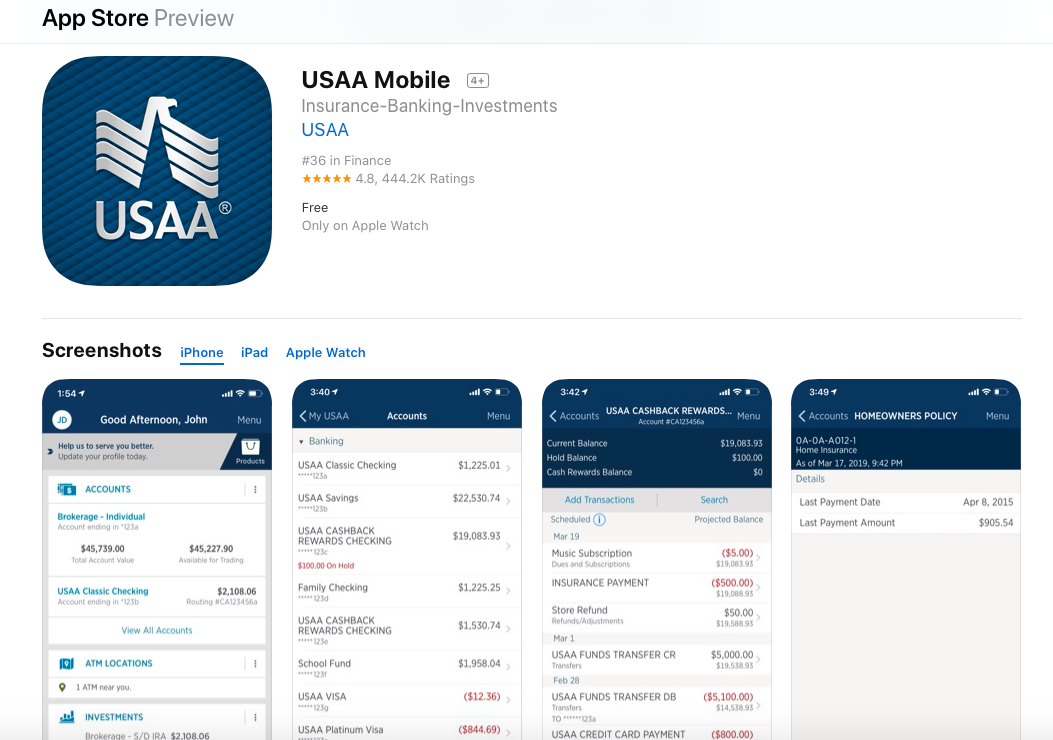

The USAA App

USAA’s mobile app is available to users from both the Google Play Store and the App Store, making it easy to take care of all your essential insurance and banking needs when you’re on the go.

The App Store Version has an impressive 4.8 out of five-star rating, based on 444.2k user ratings. Through the mobile app, you can:

- Pay bills, deposit checks, locate an ATM, calculate your loans, and more

- Request roadside assistance

- Report a claim

- Get your auto insurance ID card

- Place trades

- Get stock-quotes in real-time

- Look at your accounts and balances

The list goes on.

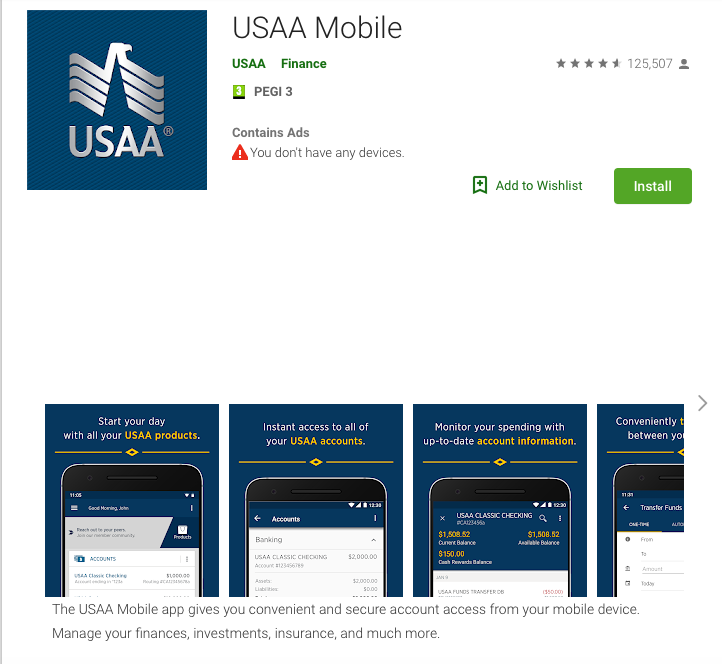

The Android version has a 4.6-star rating on the Google Play Store, based on 125,507 ratings at the time this USAA auto insurance review was written. You’ll have access to all the features noted above as you would for The App Store version.

Some users have reported that the app’s widget) which allows you to check out your balances and accounts on your device) is faulty and needs some work, showing error messages when users try to access their information. Overall, though, reviews are resoundingly positive.

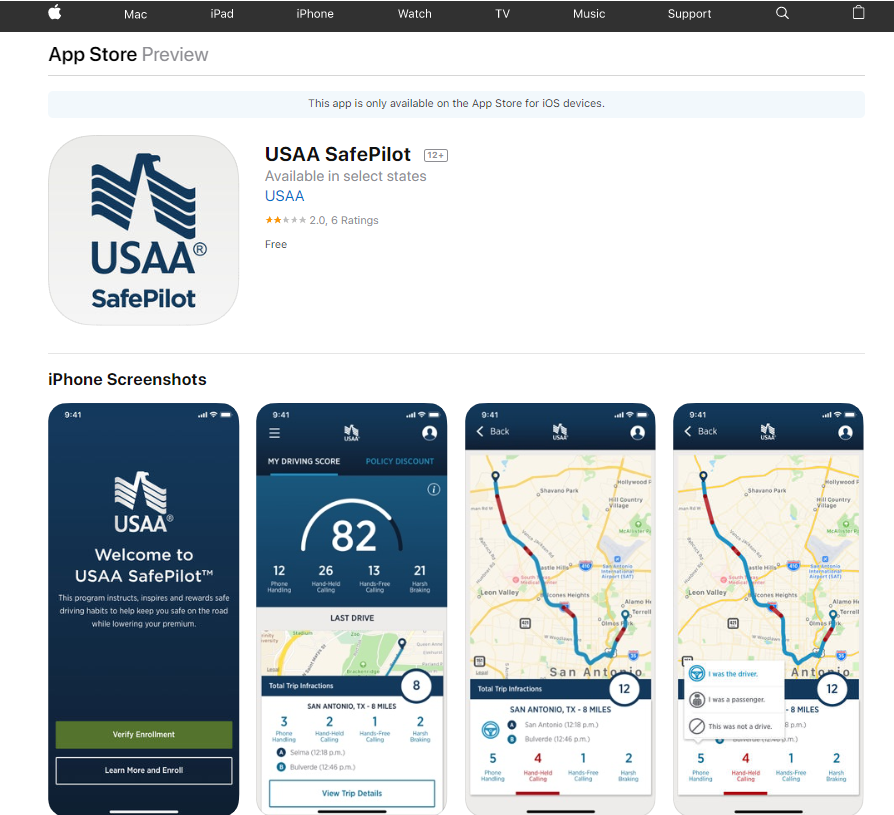

However, USAA’s usage-based driving app (SafePilot) has poor reviews.

Out of the small number of reviews that USAA’s new driving app has received, most of the negative reviews complained about the app’s availability. Most USAA customers can’t use the app because the app is only available in Arizona, Ohio, Texas, and Virginia.

Hopefully, the driving app will expand to other states in the future.

Pros and Cons

Check out the table below for a quick recap of the pros and cons from our USAA auto insurance review so you can make the best coverage choice for your driving situation.

| Pros | Cons |

|---|---|

| Available in all 50 U.S. States | Mixed consumer reviews |

| Excellent insurance ratings | Loss ratio was on the higher end between 2015 and 2017 |

| A quality selection of discounts | Moody's changed their rating in 2018 to project a negative outlook |

| Average annual rates tend to be significantly lower than the competition | Some glitches with the app |

FREE Car Insurance Comparison

Compare quotes from the top car insurance companies and save!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

The Bottom Line

What’s the bottom line? USAA offers a wide range of exceptional coverage options and has been affirmed time and time again by independent rating agencies like AM Best and S&P to be in excellent standing in terms of creditworthiness and financial stability.

USAA’s deep commitment to community and customer service is further evidenced by their ongoing work with the military, nationwide and local programs, and educational foundations.

As the data that we analyzed earlier in our USAA auto insurance review revealed, the company’s rates are by far among the cheapest offered among the top insurers in the entire country.

While some consumer reviews are mixed, the general consensus is that USAA is doing an excellent job of meeting customer’s needs, and has been doing so since its inception almost 100 years ago.

FAQ

To close out our USAA auto insurance review don’t miss our quick Q&A below to answer some of the burning questions you might still have on your mind about this carrier.

Does USAA auto insurance cover roadside assistance?

USAA’s roadside assistance coverage is part of the company’s additional protection options for consumers. With USAA roadside assistance coverage, you’ll receive aid to cover towing costs or repair expenses if the car won’t start and you’re left stranded. The coverage also covers services to deliver gas, unlock your car, or change a tire.

Does USAA auto insurance include hail damage?

If you purchase comprehensive coverage through USAA, your policy will cover a range of occurrences apart from a traditional accident or rollover, including hail damage.

Who qualifies for USAA auto insurance?

To be eligible for coverage through USAA, you must fall into one of the following categories:

- Active, retired, or honorably separated enlisted personnel or U.S. military officers

- Officer candidates enrolled in commissioning programs (such as OCS/OTS, ROTC, Academy)

- Adult children aged 18 and up of USA membres who currently have or previously had USAA property or auto insurance

- Widows or widowers of USAA members who currently have or previously had USAA property or auto insurance

How do I contact USAA?

You can reach any USAA department by calling their main number at 800-531-8722. Visit the Contact USAA page to learn more.

We hoped you found this USAA auto insurance review helpful and informative. Now, are you ready to take the next step to secure the best coverage for all the drivers in your family?

Access quotes from multiple providers with our quick, easy, and FREE online rate tool. Enter your zip code now to get started!

FREE Car Insurance Comparison

Compare quotes from the top car insurance companies and save!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Jeffrey Johnson

Insurance Lawyer

Jeffrey Johnson is a legal writer with a focus on personal injury. He has worked on personal injury and sovereign immunity litigation in addition to experience in family, estate, and criminal law. He earned a J.D. from the University of Baltimore and has worked in legal offices and non-profits in Maryland, Texas, and North Carolina. He has also earned an MFA in screenwriting from Chapman Univer...

Insurance Lawyer

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance-related. We update our site regularly, and all content is reviewed by auto insurance experts.